Life Insurance has come of age. People have adequate know how about it and have started to understand its significance in their lives. But when it comes to endowment insurance, it is no way different from life insurance. In fact, it is a part of life insurance itself. There are certain endowment plans that are designed in such a way that they award a lump sum amount post the maturity or in case of death of the policyholder. We may call endowment insurance as a plan of life insurance.

After all, they provide that much-needed comfort

Just like a life insurance policy, an endowment policy gives full amount on maturity with sum insured. In case of death, both the sum assured and bonus until the date the client has paid the premium is payable. These are also long-term plans that may mature in 10, 15 or even 20 years. But the basic difference is that the endowment plans are for a shorter duration of time whereas Life Insurance is for a longer span. Since the tenure of the endowment plan is lesser, the premiums are high. Both guarantee payouts after a specified period of time and hence are considered mostly for insurance needs.

When we talk about endowment policy, the focus is usually on its span. As discussed before, if the insured dies within the term of the policy, in that case, death benefits are provided to the beneficiaries. If in case the policyholder is still alive during the policy span then the face value gets returned to him. One of the most basic differences between the two is that in case of life insurance, upon the completion of the policy if the insured is still alive, there is no amount that is paid to the policyholder whereas in case of an endowment policy claim there is at least some amount that gets paid to the policyholder.

When it comes to premium, endowment policy premiums are slightly higher because there is a component of lump sum payment involved at the end of the policy period. Life Insurance policy premiums are lesser and are paid till the policy ends. They can be paid every month or in one shot depending on the arrangement. One can choose between participative and non-participative policies in case of life insurance. In case of an endowment policy, one can choose between unit-linked that gives profits or substantial margins.

Securing the family is what we really look out for

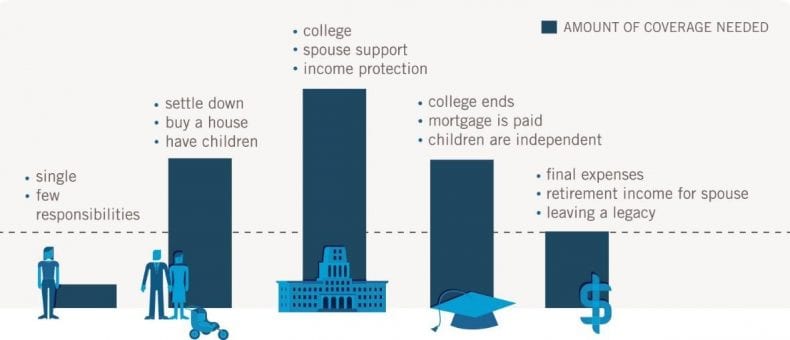

Life Insurance is about securing the future for our loved ones. Today’s era is full of unpredictability, and a sudden jolt can shake the entire family with consequences. This is where life insurance plays a very important role. It gives the much needed financial comfort at a time when the sole breadwinner for the family is no longer there. We are all aware of how important life insurance has become today. It is not only about sparing you from the income tax at the end of the financial year but has a completely different meaning to it. We must have all gone through situations where we would have found out how important a life insurance policy is. Such has been its impact that most of us today have started to spend time on deciding which policy to go for depending on our requirements and obligations. So when there is an aging spouse or other dependents, Life Insurance is the one to go for. In case, when there are plenty of liabilities on a family and then suddenly there is a sudden death of the person taking care of it, life insurance lets the family stand again on its feet and at least start from scratch. This is where we feel taking a life cover for the family is so imperative. These policies also cover the scope of the person is not able to perform his duties due to illness or permanent disability. Life Insurance if taken in a much-planned way can also take care of any loans that are in the name of the policyholder.

The various forms of endowment plans

As far as Endowment protection is concerned, this should be more customized and should take care of a certain set of requirements post the death of the policyholder. At the same time, in this case, it is not only about taking care of the family if in case there is death but also the entire policy term. Once the entire tenure is through, the policyholder, in this case, would get the endowment maturity benefit as well. That’s where his entire planning comes into the picture. There is always a need of funds at a certain age, and the endowment policy maturity amount sure takes care of it once the tenure is through. This acts as dual protection for the family as it not only provides insurance money but also gives out maturity benefits. They are indeed a kind of savings that we all look forward to having. One just needs to ensure that the premium gets paid as per the pre-decided mode, i.e., monthly, yearly or lump sum. Though the endowment policy returns may not be as lucrative as other policies but the fact that they come at a lower premium and are less risky always lets the prospect take it up. The investors who have a low appetite for risks are the ones that can always opt for this safe and secure policy. There are essentially four kinds of endowment policies-

- No Profit Endowment

- Profit Endowment

- Unit Linked Endowment

- Total Endowment

No Profit Endowment is a traditional policy that aims to give the maturity benefit to the policyholder post the tenure or provides the death benefit in case of a death.

Profit Endowment ensures that there is a lump sum amount which is paid after the death of the policyholder or in case of maturity. There is always a scope of regular bonuses involved in this type of endowment plan. This is an ideal policy in case of a mortgage as the sum assured after the maturity of the policy can always be used for paying the loan amount.

Unit Linked Endowment is a policy where part of the insurance premium is paid for the coverage, and the other half is invested in different investment options. It completely depends on the policyholder in which funds to invest.

Total Endowment is a plan where the basic maturity amount payable to the policyholder is equivalent to the death benefit, and hence the payout is relatively higher under this scheme.

There are many insurance companies that offer a range of endowment plans to its customers. Be it nationalized or private financial institutions; all know the importance of these plans offers. The best part is the acceptability as well. Most of the financial advisors always put forth endowment benefits to its customers. This is because; they can always be tweaked as per the requirements of the individual needs. The magnitude of investment in such policies can be planned in a very meticulous way just to ensure that in case of any adversity, these plans are there to bail a family out. Every financial institution offering this plan has set up its criteria when it comes to who can avail it and what can be the age of entry and maturity. The policy tenure also varies across all the companies, but at the end of the day, nowadays it is more about how fast the process is. There are some that offer more endowment returns while there are others who may not give as many returns but are more stable. It actually boils down to the preferences given by the prospect as per his requirements.

The importance of both together can never be undermined

Both in case of life insurance and endowment insurance, one is entitled to get a deduction in income tax. There are certainly other benefits as well like for example an endowment premium waiver which can always be offered to policyholders who have been regular premiums. This highlights the level of service an insurance company offers to its clients and hence always wants them to be on board. With so many insurance companies and advisors gunning for an ideal investor, it becomes very important for one to make the best selection possible. One should always ensure to go with the past track records of the companies offering life and endowment insurances as it gives a fair bit of an idea on the commitment made and the actual deliverables provided. A high percentage of claim settlement will always mean that the company is very user-friendly and hassle-free. In this ever-growing competitive market, one would always want to invest in a company which is pro-customer and takes less time when it comes to documentation as well as settling claims. Moreover, it is always advisable to go ahead with a less complicated life and endowment insurance plans because during the time of the maturity it will all boil down to how much amount one is getting and whether he is getting it in quick time or not.

Systems")

{kind=link}